- 2022-05-26 发布 |

- 21页

申明敬告: 本站不保证该用户上传的文档完整性,不预览、不比对内容而直接下载产生的反悔问题本站不予受理。

文档介绍

财务报表分析与证券估值全套配套课件英文PPT中文PPT案例教学建议Chap011.ppt

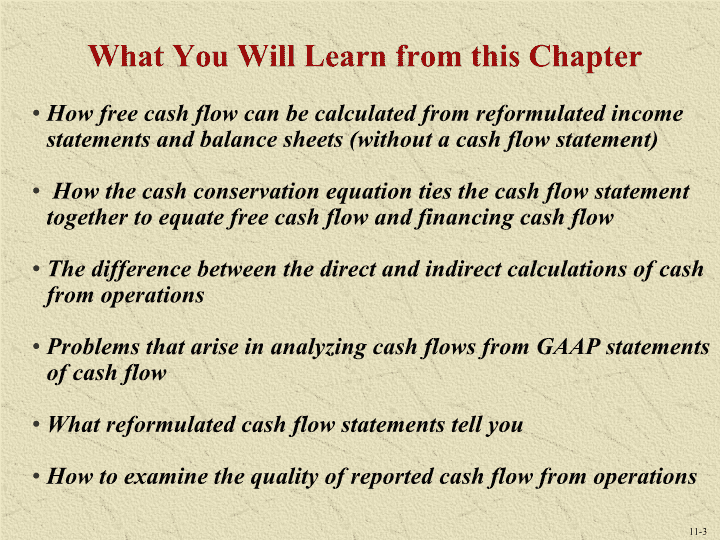

CHAPTERELEVENMcGraw-Hill/IrwinCopyright©2013byTheMcGraw-HillCompanies,Inc.Allrightsreserved. Chapter11Preparedby:StephenH.Penman–ColumbiaUniversityWithcontributionsbyNirYehuda–NorthwesternUniversityMingcherngDeng–UniversityofMinnesotaPeterD.EastonandGregoryA.Sommers–NotreDameandSouthernMethodistUniversitiesLuisPalencia–UniversityofNavarra,IESEBusinessSchool11-2 WhatYouWillLearnfromthisChapterHowfreecashflowcanbecalculatedfromreformulatedincomestatementsandbalancesheets(withoutacashflowstatement)HowthecashconservationequationtiesthecashflowstatementtogethertoequatefreecashflowandfinancingcashflowThedifferencebetweenthedirectandindirectcalculationsofcashfromoperationsProblemsthatariseinanalyzingcashflowsfromGAAPstatementsofcashflowWhatreformulatedcashflowstatementstellyouHowtoexaminethequalityofreportedcashflowfromoperations11-3 TheBigPictureforthisChapterOnceagain,appropriateanalysisdistinguishesoperatingactivitiesfromfinancingactivities--freecashflowisthefreecashflowfromoperatingactivities:thegenerationofcashflow--cashflowstoshareholdersandnetdebtholdersarefinancingactivities:thedispositionofcashflowGAAPandIFRSconfusethetwo11-4 TheCalculationofFreeCashFlowThreemethodstocalculateFCF:Usethesourcesofcashflowequation:thatis,freecashflowisoperatingincomeadjustedforthechangeinnetoperatingassetsUsethedispositionofcashflowsequation:thatis,freecashflowisnetfinancialexpenses,adjustedforthechangeinnetfinancialobligations,plusdividendstocommonshareholders.FCFcanalsobeobtainedfromthereformulatedStatementofCashFlows.11-5 CalculationofFreeCashFlow: Nike,Inc.:201011-6 TheStandardGAAPStatementofCashFlows11-7 Nike,Inc.StatementofCashFlows,201011-8 IndirectMethodforCashFlowfromOperationsNetincome+Accruals=CashfromoperationsNike’sstatement(tofollow)employstheindirectmethod(asdoalmostallfirms):2010Netincome$1,906.7millionAccruals1,257.9Cashprovidedbyoperations$3,164.211-9 DirectMethodforCashfromOperationsCashinflowsCashoutflows=Cashfromoperations11-10 ProblemswiththeStandardStatementChangeinoperatingcashshouldbeincludedintheinvestmentsection,andthechangeincashequivalentsinthefinancingsectionTransactionsinfinancialassetsareincludedintheinvestmentssectionratherthaninthefinancingsectionInterestpaymentsandreceiptsareincludedintheoperatingratherthaninthefinancingsectionTaxcashflowsareallincludedintheoperatingsection,andnotallocatedtooperatingandfinancingThestatementdoesnotincorporatenon-cashtransactions11-11 1.OperatingCashandCashinFinancial Assets:NikeChangeincashandcashequivalents$788.0millionIncreaseinoperatingcash$0.8millionIncreaseinfinancialassets787.2$788.0millionThedeterminationofoperatingcash:useanormalpercentageofsalesfortheindustry(1/2%ofsales)SeeNike’sreformulatedbalancesheetinExhibit10.3inchapter1011-12 2.TransactionsinFinancialAssets:LucentTechnologies11-13 3.NetInterestReceipts 4.TaxesonNetInterestReceipts: NikeInmillionsInterestreceipts$42.1Interestpayments(48.4)Netinterestpaymentsbeforetax6.3Taxbenefit(at36.3%)2.3Netinterestreceiptsaftertax$4.0AddbacktoGAAPCashfromOperations11-14 5.Non-cashTransactionsAcquisitionswithsharesAssetexchangesAssetsacquiredwithdebtCapitalizedleasesInstallmentpurchasesDebtconvertedtoequity11-15 ReformulatedStatementofCashFlowsThisformatfollowsthecashconservationequation:C–I=d+F11-16 TheReformulatedStatementofCashFlows: theAdjustments11-17 Nike,Inc.ReformulatedStatementofCashFlows11-18 WhyFreeCashFlowfromAdjustedCashFlowStatementsMaynotReconciletotheMethods1and2“Otherassets”and“otherliabilities”arenotidentifiedaseitheroperatingorfinancingCashdividendsinthecashflowstatementdifferfromdividendsintheequitystatementCashfromshareissuesinthecashflowstatementmaydifferfromshareissuesintheequitystatementDetailsforadjustments3,4and5arenotavailableGAAP’streatmentofemployeestockoptions(Chapter9)Cashflownumbersofforeignsubsidiariesaretranslatedataverageexchangerateswhereasbalancesheetnumbersaretranslatedatend-of-yearexchangerates11-19 TheCalculationofCashFlowfromOperationsThepracticalmatterofdistinguishingcashflowfromoperationsfromcashflowfrominvestmentactivitiesisnotaneasyone:thecashflowfromoperationsintheGAAPstatementisnotacleanmeasure.SomecashflowsfrominvestmentactivitiesareclassifiedascashflowsfromoperationsR&DexpendituresInvestmentininventoriesTaxesongainsfromassetssalesareclassifiedascashflowfromoperationsNote,however,thatforacalculationofFCF(C–I),amisclassificationbetweeninvestmentandoperatingactivitieshasnoeffect11-20 TheQualityoftheReportedCashFlowfromOperations(CFO)NumberNoncashchargesdonotaffectCFO,butarealossofvalue(e.g.depreciation)FirmscandelaypaymentstogeneratecashflowFirmscansellreceivablestogeneratecashflowFirmscanreduceadvertisingexpenditurestogeneratecashflowFirmscanreduceR&DexpenditurestogeneratecashflowNon-cashtransactionsarenotinCFOStructuredfinancingcanmakeborrowinglooklikecashfromoperationsCapitalizationpolicyshiftsCFOtocashinvestment11-21查看更多